Weekly Market Update – 7 October, 2022

In the US, Fed policymakers restated on Tuesday that taming inflation remains a serious problem, and “may take some time” to address, but policymakers they are resolute to “bring inflation back down to 2%”. These remarks come two weeks after the Fed raised rates by another 75bps to the current level of 3.00-3.25%. That rate is expected to be 4.6% by early next year. Markets currently expect another 75bps hike in the next policy meeting to be held November 1-2.

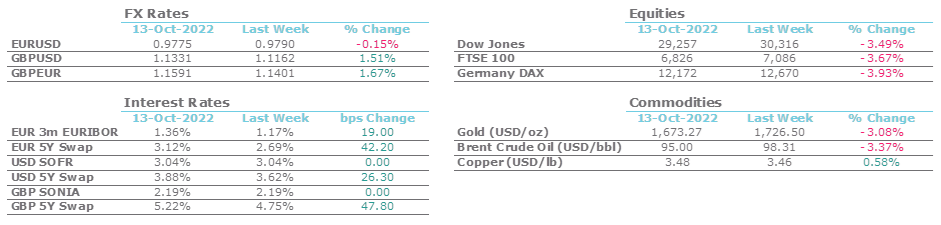

The euro rose approximately 0.3% this week nearing parity with the dollar, but later fell to the current trading rate of $0.98. GBPUSD had a similar performance this week, rising slightly and later falling to the current rate of $1.12 albeit still up from the low of $1.07 last week.

The Reserve Bank of Australia surprised this week raising rates by 25bps (vs 50bos expected) renewing discussions around diverging policies and whether other central banks may also temper tightening soon. The Australian dollar is now trading near recent lows at $0.64.

Oil prices hit a near three-week high (WTI $89) following the news that OPEC+ agreed to tighten global crude supply by cutting production targets by 2 million barrel per day in the largest reduction seen since 2020.

Currency, commodity and rates volatility is impacting clients both at Fund and Portfolio levels. We continue to guide clients In developing hedge strategies and implementing these in a very uncertain and illiquid environment.

This week’s big movers