Weekly Market Update – 14 October, 2022

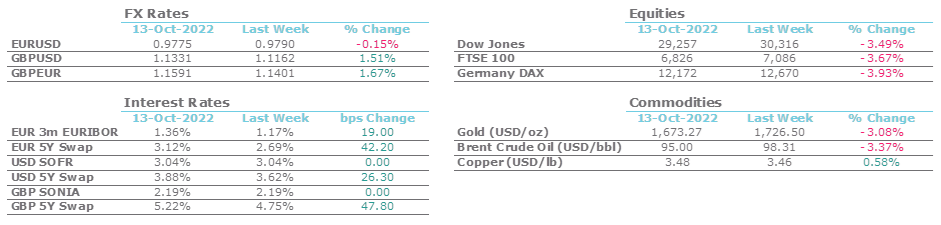

Yesterday, the September core US CPI came in above expectations with the YoY rate reaching 6.6%, the highest level in the last 40 years and showing that the fight to bring inflation down to target levels is far from over. With these figures, economists expect the Fed to press on with its aggressive tightening programme with an expected 75 bp increase at the next meeting in early November. USD 5y swap rates increased by 10 bp to 3.90% after the announcement.

The UK Government is preparing to drop a central part of its aggressive tax-cutting plan, following weeks of turmoil in financial markets. Media speculation of a U-turn on parts of the UK mini-budget pushed gilts and swap rates down 50 bp as institutional investors remain nervous after the BoE backed its commitment that the emergency gilt buy-back scheme would end this Friday. By contrast USD & EUR swap rates remained high (USD 5y rate 3.90%, EUR 5y rate 3.04%). 6-month EURIBOR fixed above 2% this week for the first time since 2009.

The pound gained 2.6% against the EUR at 0.8640, the strongest it has been for over a month, and 2.74% against the USD at 1.1272. The USD-JPY continued higher (up to 147.75 at time of writing) and other emerging markets currencies remain under pressure with USD-INR holding in the 82 area and USD-CNH back above 7.20.

With the current EURUSD still well below parity at 0.9735, PMC continues to assist financial sponsors with analysing and potentially hedging USD exposures.